Upgraded Cards, Upgraded Insights

Joe Agostinelli, Research and Analytics, Vibrant Credit Union

Joe Agostinelli, Research and Analytics, Vibrant Credit Union

However, I really believe getting our cards in the mobile wallets of our members is going to be one of the more “sticky” things we can do moving forward. And getting those deep relationships with our members is what will help us continue to grow and maintain a strong offering as opposition across financial services mounts.

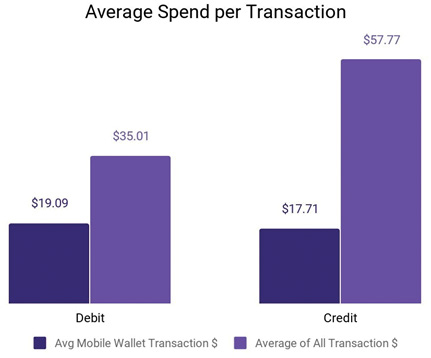

What about the actual transactions?

Vending and Quick Serve Food are the top usage categories which obviously consist of lower dollar transactions. These two are followed by Grocery and Large Retailer categories. This isn’t a bad thing, but it speaks to where these mobile wallets are NOT being used at this point...airline travel, car rentals, warehouses possibly, and hotels.

Apple: Best in Class

From our data, Apple Pay is clearly the dominant player in the market at this point even though their phone market share is fairly equal with Samsung.

Apple is upping the ante soon by offering their own credit card. Although it may not be a complete game changer, financial institutions will certainly be looking to (re)act quickly once the card launches. Apple has a really cool looking titanium card that will be a “status” card wherever the cardholder has a chance to flash it. However, the physical card can’t be the main focus for Apple, the creator of the Apple Wallet.

I don’t know what their onboarding process will look like, but if I were them, I would smack that card directly into every Apple Wallet out of the gate and put it in the top position. Maybe even delay delivery of the physical card a day or two to encourage mobile wallet usage.

What does this all mean?

As we dig further into the data, I’m sure we will see some trends in shopper behaviors by device. Where do people with iPhones shop vs. Samsung? This may take a little while to vet out, but could lend to some cool insights down the road.

There are still several things that are going to drive transaction usage via the mobile wallet in the near future:

1. Consumer adoption and comfort with this method

2. Merchant acceptance continuing to grow

3. If possible, figuring out how to leverage this method for all types (especially higher dollar) purchases

We still have a lot of work to do as an organization to get our arms fully around this data, but being able to react so quickly out of the gate has allowed us to upgrade the knowledge we have about our members and how to better serve them moving forward.

Apple is upping the ante soon by offering their own credit card. Although it may not be a complete game changer, financial institutions will certainly be looking to (re)act quickly once the card launches. Apple has a really cool looking titanium card that will be a “status” card wherever the cardholder has a chance to flash it. However, the physical card can’t be the main focus for Apple, the creator of the Apple Wallet.

I don’t know what their onboarding process will look like, but if I were them, I would smack that card directly into every Apple Wallet out of the gate and put it in the top position. Maybe even delay delivery of the physical card a day or two to encourage mobile wallet usage.

What does this all mean?

As we dig further into the data, I’m sure we will see some trends in shopper behaviors by device. Where do people with iPhones shop vs. Samsung? This may take a little while to vet out, but could lend to some cool insights down the road.

There are still several things that are going to drive transaction usage via the mobile wallet in the near future:

1. Consumer adoption and comfort with this method

2. Merchant acceptance continuing to grow

3. If possible, figuring out how to leverage this method for all types (especially higher dollar) purchases

We still have a lot of work to do as an organization to get our arms fully around this data, but being able to react so quickly out of the gate has allowed us to upgrade the knowledge we have about our members and how to better serve them moving forward.

As We Dig Further Into The Data, I’m Sure We Will See Some Trends In Shopper Behaviors By Device. Where Do People With Iphones Shop Vs. Samsung?

Apple is upping the ante soon by offering their own credit card. Although it may not be a complete game changer, financial institutions will certainly be looking to (re)act quickly once the card launches. Apple has a really cool looking titanium card that will be a “status” card wherever the cardholder has a chance to flash it. However, the physical card can’t be the main focus for Apple, the creator of the Apple Wallet.

I don’t know what their onboarding process will look like, but if I were them, I would smack that card directly into every Apple Wallet out of the gate and put it in the top position. Maybe even delay delivery of the physical card a day or two to encourage mobile wallet usage.

What does this all mean?

As we dig further into the data, I’m sure we will see some trends in shopper behaviors by device. Where do people with iPhones shop vs. Samsung? This may take a little while to vet out, but could lend to some cool insights down the road.

There are still several things that are going to drive transaction usage via the mobile wallet in the near future:

1. Consumer adoption and comfort with this method

2. Merchant acceptance continuing to grow

3. If possible, figuring out how to leverage this method for all types (especially higher dollar) purchases

We still have a lot of work to do as an organization to get our arms fully around this data, but being able to react so quickly out of the gate has allowed us to upgrade the knowledge we have about our members and how to better serve them moving forward.

Weekly Brief

Read Also

Navigating Compliance Challenges in ESG AML and Digital Onboarding

Chuan Lim Ang, Managing Director and SG Head of Compliance, CIMB

A Vision for the Future: Automation, Robotics, and the Smart Factory

Joe Tilli, State Industrial Automation Sales Manager, Lawrence & Hanson

The Rise of Hyper Automation

Erdenezaya Batnasan, Head of IT End-User Support Service Department, Khan Bank

Transforming Business Operations with Robotic Process Automation

Simon So, CMGR, MCMI, Regional Head of Digital Solutions, Richemont Asia Pacifi

Combining Automation with AI to Achieve Human-Like Interaction

Kain Chow, General Manager, Technology & Transformation, New World Development Company Limited

Implementing RPA - 5 Ultimate Prerequisite

Indra Hidayatullah, Data Management & Analytics Division Head, Pt. Bank Tabungan Negara

Incorporating the power of recognition into our vendors' sustainability journey

Cynthia Khoo, Head, Central Procurement Office, OCBC Bank (Malaysia) Berhad

Elevating Guest Experience with Data

Clive Edwards, Senior Vice President, Operations, Capella Hotel Group